5 Questions for 2021

The pandemic changed the way we live, work and entertain ourselves. There is little doubt that vaccine distribution will be among the most important macroeconomic variables of 2021, but advance knowledge of vaccination rates would not be sufficient to predict where the economy or asset prices will finish in 2021. Additional questions need to be answered.

In a new Global Insights report, Jason Thomas, Head of Global Research, outlines the top 5 questions for global investing in 2021. Review the key themes Jason highlights in the report and download the full version below.

5 Questions for 2021

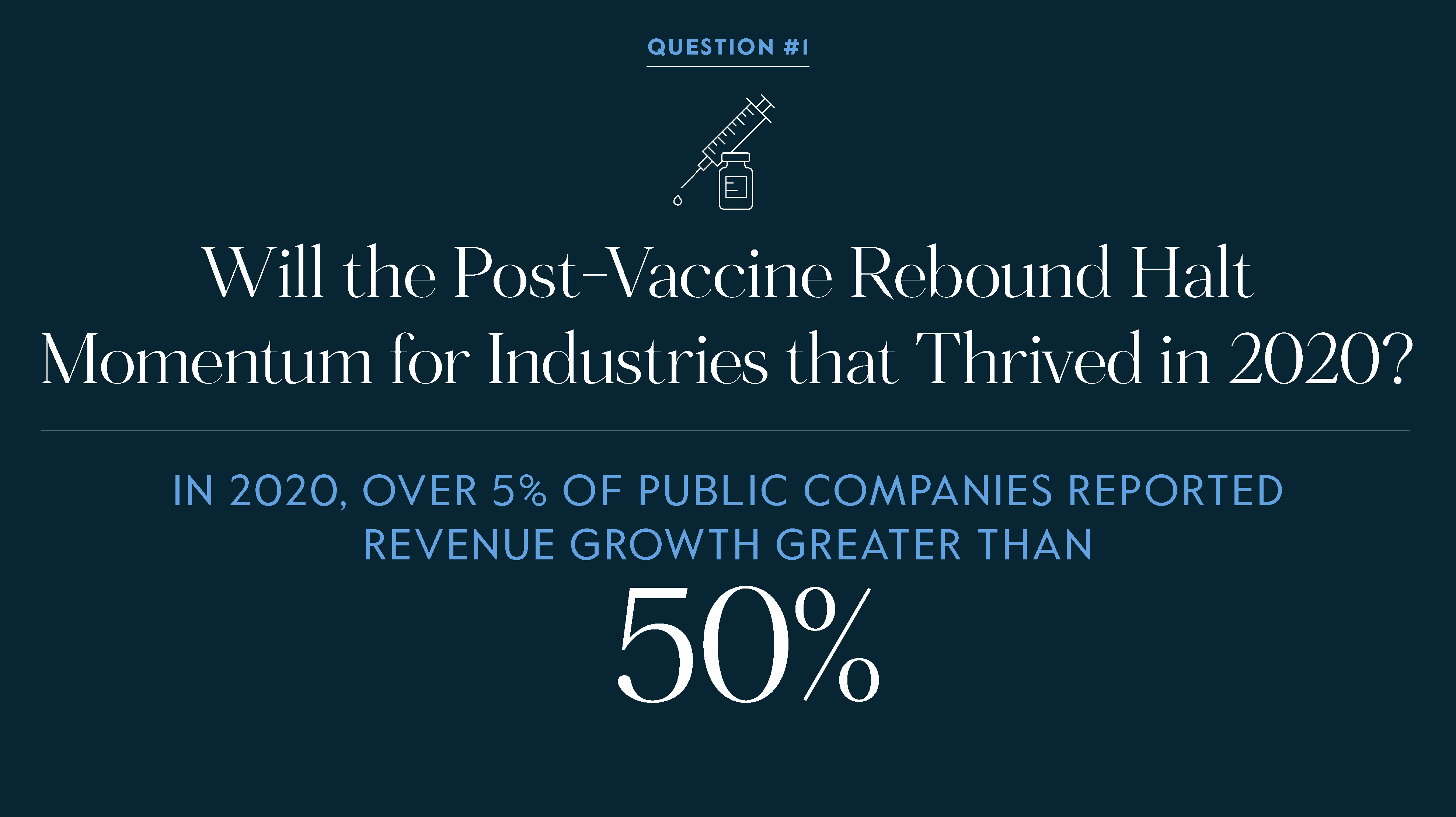

Will the post-vaccine rebound halt momentum for industries that thrived in 2020?

In 2020, savings from sharply reduced services spending financed a boom in digital media and durable goods purchases. Will the post-vaccine environment see a rebound in hard-hit categories such as travel, hospitality, and entertainment at the subsequent expense of 2020’s pandemic “beneficiaries,” or will pandemic-induced lifestyle changes prove to be more persistent than expected?

Source: Measured on a year-over-year basis to trough in activity. Greenwood, R. et al. (2020), Sizing Up Corporate Restructuring in the COVID Crisis,” NBER Working Paper 28104.

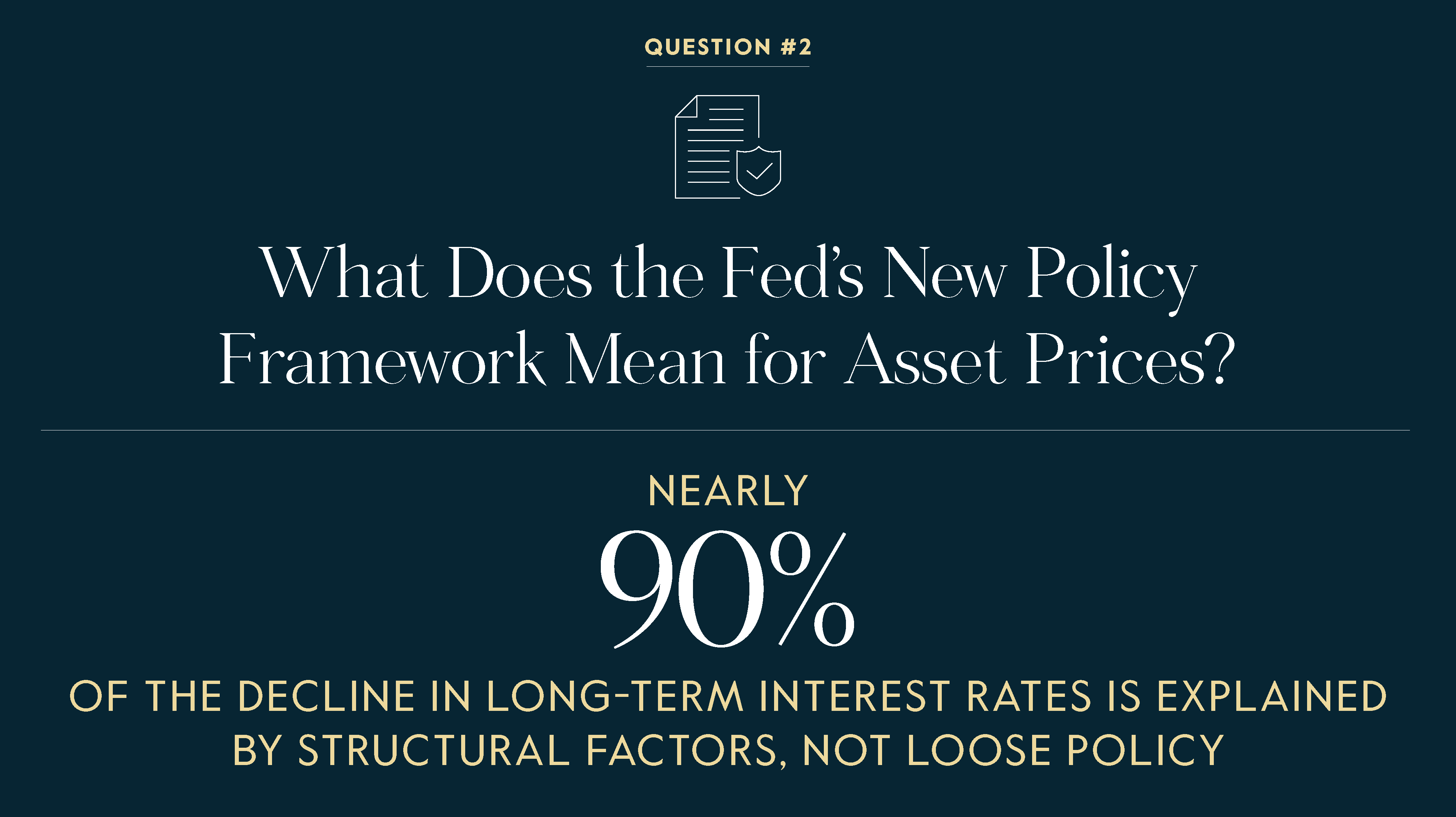

What does the Fed’s new policy framework mean for asset prices?

Lower (real) interest rates boost asset prices by depressing the discount rates applied to all future cash flows. With asset prices so leveraged to low rates, should investors worry about a sudden and unforeseen change in monetary policy?

Source: Carlyle Analysis of Ken French, U.S. Treasury Data, 2020. There is no guarantee any trends will continue.

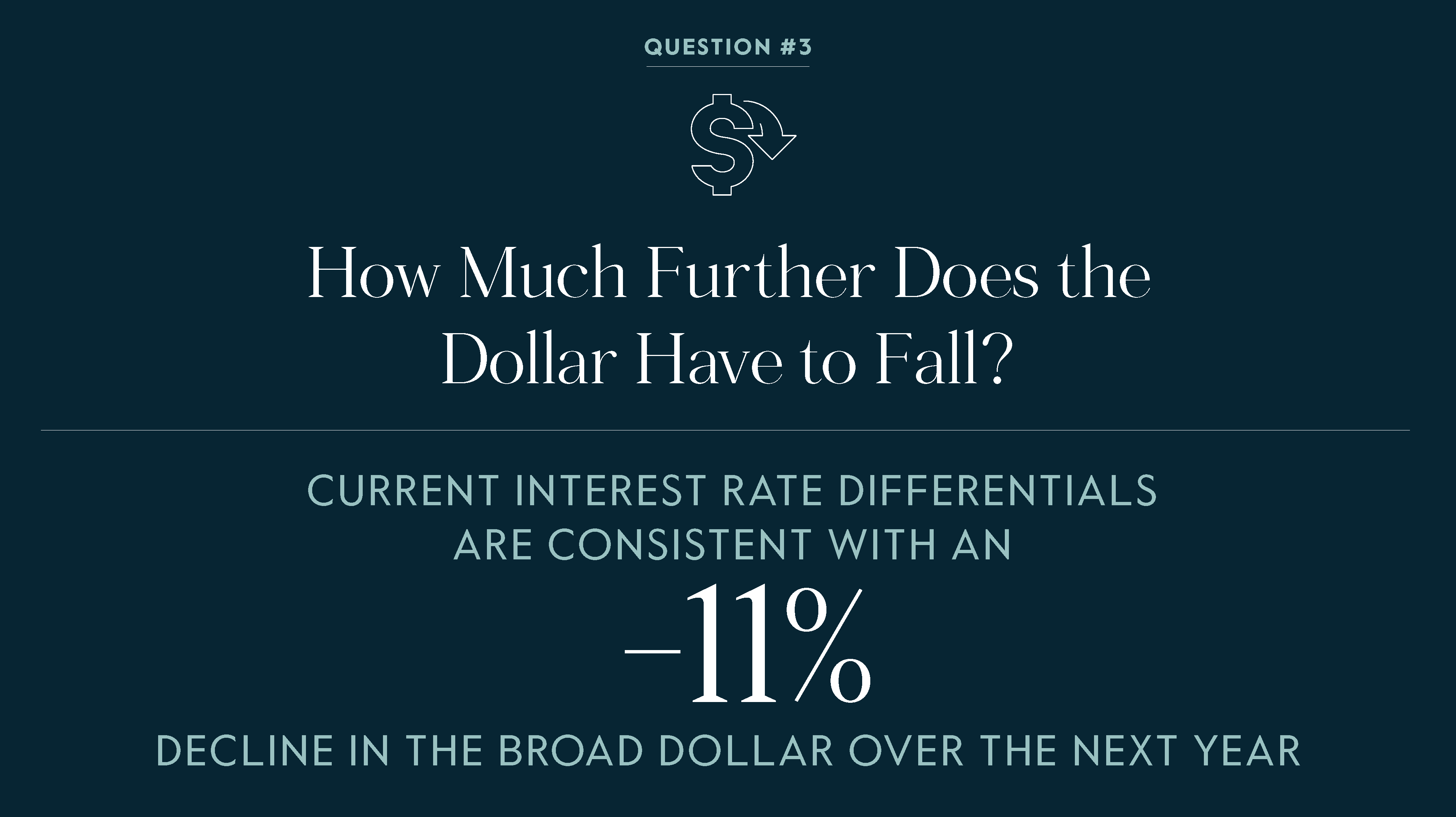

How much further does the dollar have to fall?

During the Fed’s last tightening cycle, the differential between U.S. interest rates and those in the rest of the world widened by nearly 350bps, driving a 35% appreciation in the dollar against a broad basket of currencies, pressuring EM borrowers and increasing the cost of U.S. workers on a relative basis even as wage appreciation remained tepid. If adopted, a coordinated fiscal-monetary depreciation of the dollar could support both domestic wage inflation and bolster EM corporate finances.

Source: Carlyle Analysis; BEA and Federal Reserve Board Data, January 5, 2021.

Has China’s relative economic position strengthened?

Successful containment of the coronavirus and strongly entrenched manufacturing and logistics infrastructure catapulted China to a quick rebound after a sharp contraction in Q1-2020. The path of its future growth trajectory is clouded by the shift towards domestic demand, and potentially diminished access to technologies and digital markets.

Source: Carlyle Analysis. IMF, WEO Database, October 2020.

What do migratory patterns suggest about the future of work and state finances?

In the U.S., as the pandemic dragged on and “back-to-the-office” imperatives diminished, people not only fled cities for suburbs but also left many major metro areas entirely, with significant out-migration from New York, Chicago, and California. Will the ongoing exodus from crowded and high-cost metro areas force employers to embrace remote work to compete for talent, exacerbating the slump in high-density markets?

Source: Carlyle Analysis; Federal Reserve Bank of St. Louis. Census Bureau. There is no guarantee these trends will continue.

Read 5 Questions for 2021 by Jason Thomas

ABOUT THE EXPERT

Jason Thomas is the Head of Global Research at The Carlyle Group, focusing on economic and statistical analysis of Carlyle portfolio data, asset prices and broader trends in the global economy. He is based in Washington, DC. Mr. Thomas serves as Economic Adviser to the firm’s corporate Private Equity, Real Estate and Credit Investment Committees. His research helps to identify new investment opportunities, advance strategic initiatives and corporate development, and support Carlyle investors. Prior to joining Carlyle, Mr. Thomas was Vice President, Research at the Private Equity Council. Prior to that, he served on the White House staff as Special Assistant to the President and Director for Policy Development at the National Economic Council. In this capacity, Mr. Thomas served as primary adviser to the President for public finance. Mr. Thomas received a BA from Claremont McKenna College and an MS and PhD in finance from George Washington University, where he studied as a Bank of America Foundation, Leo and Lillian Goodwin Foundation, and School of Business Fellow. Mr. Thomas has earned the chartered financial analyst designation and is a Financial Risk Manager certified by the Global Association of Risk Professionals.